Will the Bark be worse than the Bite?

This is the question that I keep asking myself. Over the past few weeks, the bond market experienced one of the largest declines since 1980. For the first quarter of the year, the Bloomberg Aggregate Bond Index declined by almost 6%. That loss of value includes earned interest, so you can imagine the declines experienced by investors owning bond funds if they didn’t reinvest the dividends. This heightened volatility has not been confined to the bond market either. The broader equity benchmarks declined between 4.6% on the S & P 500 to 8.9% on the Nasdaq 100 in the first quarter of this year.

Obviously, the Fed is just one of several worries facing investors today. The war in Ukraine is the dominant news story along with inflation hitting a 40-year high. More recently, COVID outbreaks have led to new lockdowns in parts of Asia, and we assume these lockdowns will only add to supply chain issues for American and European consumers. Still, the question that weighs most heavily on my mind is what the Fed will do this year.

Despite the current uncertainty, we are optimistic about the next few quarters for reasons stated in the rest of this letter. Simply put, we think inflation will gradually fall back towards normal levels. As that happens, we think the Fed will also tone down its rhetoric and actions, though inflation will continue to erode the purchasing power of cash. While there is always the possibility of a recession, the average American and our banking system are much stronger financially than fifteen years ago when a housing slowdown created a major economic downturn.

While this letter discusses our views on inflation and the economy, we do not manage portfolios based on our macro-economic forecasts. We are business buyers focused on fundamental quality and value. Fortunately, our strategy naturally favors high-quality businesses with pricing power that tend to outperform during weaker economic periods and in years when real interest rates are rising. So, the Fed tightening monetary policy isn’t necessarily a negative for our portfolios. Obviously, we would prefer an environment of prosperity and stability, but our disciplined approach focuses on the business fundamentals regardless of the news.

First, we think it is worth noting that interest rates have been artificially low for a very long time. We own many companies that could benefit from moderately higher interest rates if the Fed is able to do so without triggering a recession. A bank is a good example of a business that generally benefits from higher interest rates, especially when the yield curve is positively sloped (interest rates rise as the length of the loan or deposit is increased). Those conditions allow the bank to charge more for a loan, such as a mortgage, than it is paying for its deposits (checking, savings, CDs). Over the past decade, banks have steadily grown their non-borrowed reserves as interest rates hovered near zero, and currently have almost $4 trillion in excess reserves. Our view for the past year has been that rising inflation would eventually move interest rates back to a more normal level, and that expectation was a major factor in the timing of our M & T Bank purchase in early 2021. We expect higher rates will also improve interest earnings and lending.

“During scary periods, you should never forget two things: First, widespread fear is your friend as an investor because it serves up bargain prices. Second, personal fear is your enemy.”

— Warren Buffett

Second, it is important to remember the definition of inflation as well as the primary drivers of the current spike in prices. Over the past week, we have seen inflation readings as high as 11.2% for the producer price index. That number represents a 12-month change and includes energy prices that have spiked wildly since Russia invaded Ukraine. Additionally, recent inflation has been amplified by supply chain issues in Asia. Finally, inflation is being pushed higher by wage gains throughout our society.

It is important to remember that inflation is the rate of change, not the actual price of goods. So, inflation could moderate back to a more normal level over the next few quarters even as prices continue to rise if prices simply rise at a slower pace. We don’t need wages and prices to go down for inflation to fall back to a normal level, but for them to simply rise less quickly.

The scenario where inflation naturally moderates is a very real possibility when we look at the factors contributing to recent inflation. The Fed’s hawkish commentary along with the March 16th rate hike have already moved interest rates higher in parts of the economy. According to an April 14th article in the Wall Street Journal, the 30-year mortgage rate topped 5% in the past week for the first time in more than a decade. That is a significant jump in rates that seems likely to cool the housing market. Perhaps as an early indication of that effect, Bloomberg reported this week that lumber prices have now fallen 30% since the beginning of March.

Likewise, the war in Ukraine has created a surge in food and energy prices around the world. Higher prices for these commodities should abate over the next year regardless of the outcome in Ukraine. If oil and gas prices stay elevated, then we should see new investments in energy production in other places like North America. Higher agricultural prices are likely to spur additional production in other parts of the world where they need higher prices to be profitable. Finally, we think it is only logical to assume that factories in Asia and global supply chains will eventually return to full capacity.

As these possible outcomes materialize, inflation should ease back towards the normal historical range (60-year average 3.2%). If the inflation readings moderate, we expect the Federal Reserve to become less hawkish. Keep in mind, this scenario still involves higher inflation than we’ve seen in recent years and higher interest rates. However, it isn’t the worst-case scenario. We own many businesses that can prosper in an environment of moderate inflation and normal interest rates, and a reasonable level of inflation is good for the economy.

Key Charts & Supporting Data

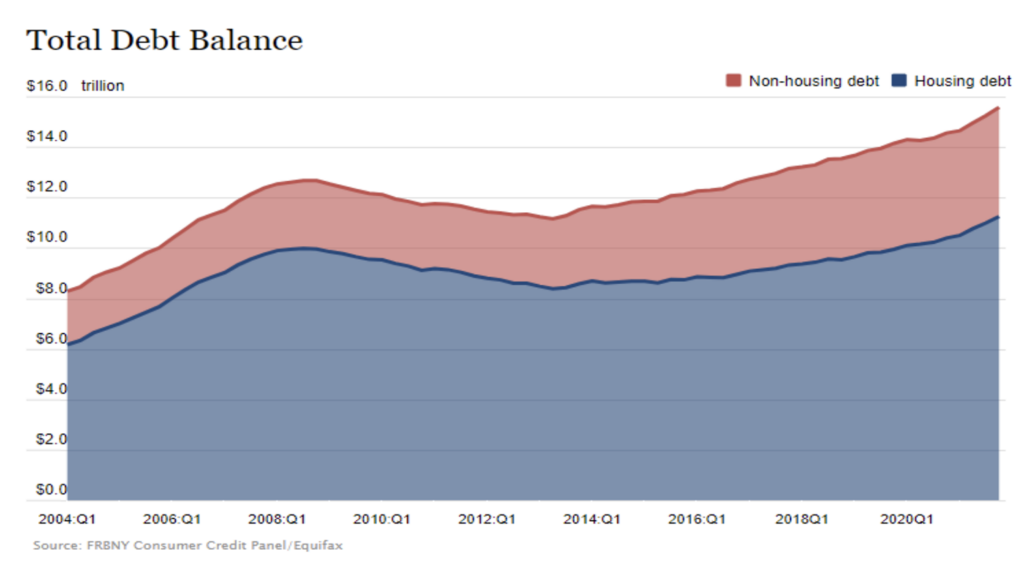

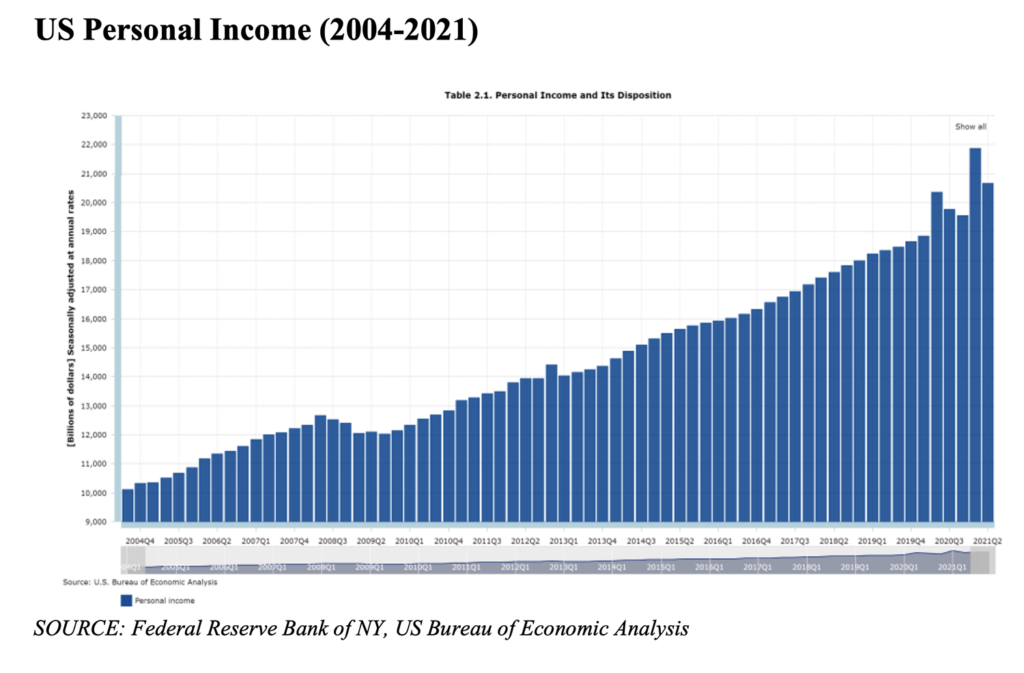

Despite the frothy housing market of the past few years, American consumers—in aggregate—are in a much stronger financial position than they were fifteen years ago. As illustrated in the chart below, housing-related debt peaked at approximately $10 trillion in 2008 and did not exceed that level again until 2020. During that same twelve-year period, the size of the U.S. economy (GDP) grew by roughly 50%, and aggregate personal income increased by a similar amount.

Household net worth has grown even more dramatically, rising from roughly $67 trillion at its 2007 peak to more than $140 trillion by the end of 2021. In summary, the average American today has meaningfully higher income and asset levels than in 2008, while overall debt has increased only modestly. Although these factors do not eliminate the risk of a recession, we believe they should help limit both the depth and duration of the next economic downturn.

“Money will always flow toward opportunity, and there is an abundance of that in America. Commentators today often talk of ‘great uncertainty.’ But think back, for example, to December 6, 1941, October 18, 1987, and September 10, 2001. No matter how serene today may be, tomorrow is always uncertain.”

— Warren Buffett

In closing, I want to reiterate what I have discussed above:

- While it is possible that they will act too aggressively and push the country into a recession, we do not think that is the most likely outcome. The Fed, largely through its comments more than its actions, has already moved the bond market dramatically.

- Inflation has recently registered numbers not seen in forty years, but we do not think the current inflationary spike will be a persistent issue like that seen in the 1970’s. There are catalysts driving some of the current inflation readings that should logically moderate in the coming months.

- Inflation can ease back to a more normal range without prices going down. If wages and other prices continue to rise, but at a slower pace, then inflation will decline. If some commodity prices, such as oil or lumber, decline in price, then inflation should moderate even more quickly.

- We own high-quality businesses that possess strong pricing power characteristics, which should allow them to raise prices as inflation pushes through their business models. For companies with pricing power, inflation simply contributes to revenue growth as they raise prices.

- Additionally, we actively manage portfolios with a value bias looking for opportunities created by market volatility. As such, we can make more attractive purchases when other investors behave emotionally. Over the past few weeks, we have made additional buys into strong global businesses such as Louis Vuitton, Nike, T. Rowe Price, Analog Devices, and J.P. Morgan for clients at steep discounts to the prices those stocks commanded just last year. We are using fear and uncertainty as an opportunity to add to high-quality businesses, and we believe we will be rewarded over time.