(Especially when the ice looks thin)

Through the end of October, our average return since the beginning of the year for most clients is approaching 20%. Despite those gains, this year has been challenging at times for disciplined investors like us.

Our investment strategy has evolved over the past 25 years, but the core objectives have remained the same. We own high-quality businesses that have the potential to grow while also possessing a margin of safety, such as a discounted valuation or a dominant brand. By focusing on quality and value, we expect our portfolios to perform solidly during good markets, while experiencing drawdowns that are shallower in magnitude and shorter in duration than the overall stock market during tougher years.

Historically, this has been true for investors with strategies like ours, including our long-term clients who came through the tech bubble with us. In addition, our focus on companies with a consistent track record of raising dividends provides our clients with income during those drawdowns. However, the tradeoff for owning dividend-paying stocks—which often lose less and recover faster—is that we do not fully participate in the upside when Mr. Market’s mood drifts toward euphoria.

The good news is that we are finding many attractive opportunities in our investment universe today. At the same time, there are considerable risks that many investors may be ignoring in their pursuit of index-beating returns. Market valuations, particularly for technology stocks, have moved into levels not seen since the peak of the dot-com bubble. The Nasdaq 100 was trading at 43 times earnings at the end of the third quarter. If not for Apple and Microsoft—the two largest holdings in the index—valuations would be even higher.

Research published by Bernstein in September reported that technology stocks among the 1,500 largest companies in the country are now more expensive than at any point other than 1999 over the past 50 years, based on market value to sales. As one example of investor optimism, Tesla currently has a fully diluted market value of approximately $1.5 trillion—greater than all traditional automakers combined—despite having only a 1% share of the global auto market.

Macro-Economic Conditions and Concerns

We find ourselves at an interesting moment for the global economy and for investors across every asset class. As the world slowly emerges from the coronavirus pandemic, there are a number of potential risks that could be significant for both investors and consumers. The most concerning risks, in our view, include potential sources of inflation, downward pressure on profitability and productivity, and the possibility of higher taxes.

Key risks we are monitoring include:

- Central banks have been exceptionally accommodative over the past several years. Based on this week’s press release from the Federal Reserve Open Market Committee, it appears we may be nearing an inflection point in that liquidity. Moments like this in history have often created opportunities for policy mistakes. While bond yields have moved modestly higher, global interest rates remain near 60-year lows—meaning bond prices are still near all-time highs.

- Global supply chains have been a major source of productivity gains and cost savings over the past four decades, as manufacturing systematically shifted from one low-cost country to another. The pandemic exposed the fragility of those supply chains, and we are now seeing the first signs of input-cost inflation in decades.

- Wage inflation has been minimal for much of the past 40 years, with most wage gains driven by productivity improvements and innovation, particularly among higher-income workers. The pandemic may have disrupted that trend. An extremely tight labor market, combined with fiscal stimulus, has given many lower-income workers greater bargaining power to demand higher pay. The tradeoff for higher wages is either lower corporate profits or higher inflation.

- While it is still too early to be certain, there are signs that the long-term downward trend in tax rates that began during the Reagan era may be ending. Corporate tax rates appear most at risk for increases, especially for large global technology companies that have historically benefited from very low average tax rates.

We do not invest based on macroeconomic forecasting, but we do consider how these potential outcomes could negatively impact our investments. The risks outlined above could lead to reduced profit margins and slower economic growth. Despite these potential headwinds, most asset classes continue to trade at or near record highs.

Fortunately, our investment decisions are grounded in the quality of the businesses we own, the opportunities we see in their current share prices, and the downside risk we perceive if those opportunities fail to materialize. Simply stated, we aim to be handsomely rewarded when our thesis proves correct, while limiting downside if it does not.

We also benefit from owning a smaller, more focused portfolio of unique opportunities, rather than hundreds of stocks or bonds that simply mirror the broader market. For example, our portfolios have significantly greater exposure to the global consumer and to currencies other than the U.S. dollar. Many of these foreign companies trade at meaningful discounts to their U.S. peers, even though they often have stronger balance sheets and greater exposure to the fastest-growing economies in the world.

Additionally, the average company we own is roughly half the size of those held in major indices. While being smaller does not guarantee higher growth, smaller companies have historically been able to grow earnings at a faster pace than their larger peers.

“Investing is about preserving more than anything. That must be your first thought—not looking for large gains. If you achieve only reasonable returns and suffer minimal losses, you will become wealthy and will surpass any gambler friends you may have. Considering the downside is the single most important thing an investor must do.”

— Irving Kahn

Studied under Benjamin Graham and worked on Wall Street for 86 years

We do not invest based on macroeconomic forecasting, but we do consider how certain potential outcomes could negatively impact our investments. The issues discussed above could lead to reduced profit margins and slower economic growth. Despite these potential headwinds, most asset classes are currently trading at or near record highs.

Fortunately, our investment decisions are grounded in the quality of the businesses we own, the opportunities we see in their current share prices, and the downside risk we perceive if that upside opportunity fails to materialize. Simply stated, we want to be handsomely rewarded if our thesis proves correct, while limiting downside if it does not.

We also benefit from owning a smaller, more focused portfolio of unique opportunities, rather than hundreds of stocks or bonds that merely act as proxies for the overall market environment. For example, our portfolios have significantly greater exposure to the global consumer and to currencies other than the U.S. dollar. Many of these foreign companies trade at meaningful discounts to their U.S. peers, even though they often have stronger balance sheets and greater exposure to the fastest-growing economies in the world.

Additionally, the average company held within our portfolios is roughly half the size of those included in major indices. While being smaller does not guarantee higher growth, smaller companies have historically been able to grow earnings at a faster pace than their larger peers.

Benchmarks and Market History

We are often asked how our strategy performs relative to the S&P 500 Index. The S&P 500 is comprised of 505 companies and is market-cap weighted, meaning the 10 largest technology companies represent approximately 30% of the overall index.

The goal of beating the index tends to be most popular during prolonged bull markets, yet the benchmark has also experienced multiple extended periods of zero returns over the past century. Our clients have hired us to help protect their nest eggs throughout their lifetimes—specifically against the destructive impact of inflation—as they expect these assets to generate income during retirement.

That means we are consistently focused on owning assets with the potential to produce real returns (net of inflation), either above a client’s desired withdrawal rate or sufficient to fund future goals. After a decade of robust index returns, we believe many investors underestimate both the depth and duration of prior drawdowns that have followed similar periods.

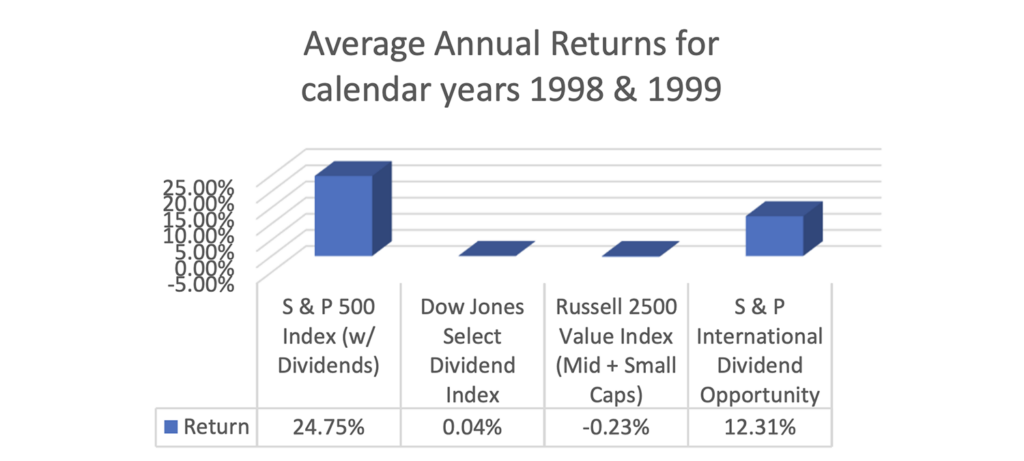

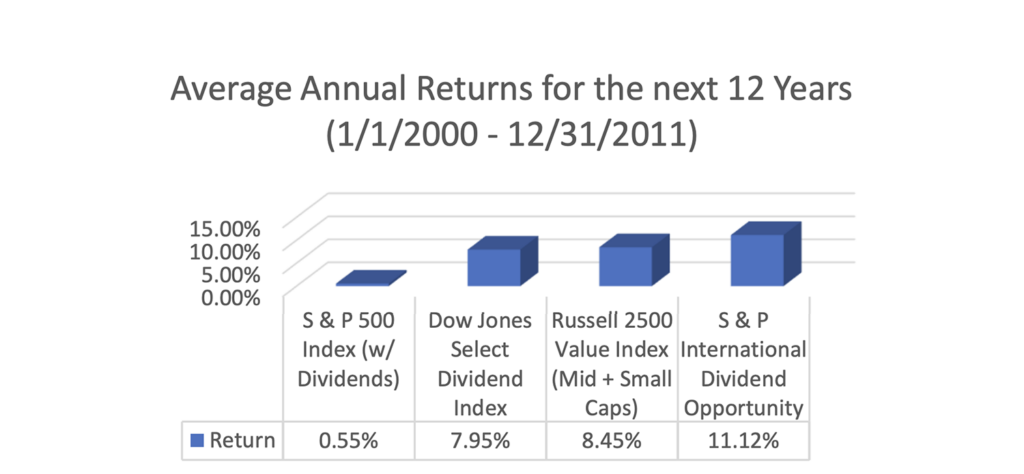

The charts below show average annual returns for the S&P 500 Index compared to three dividend- or value-oriented indices at the end of the tech bubble and over the subsequent 12 years. Our holdings more closely resemble a combination of these three benchmarks, as we own companies of varying sizes—both domestic and foreign—with an emphasis on dividends and valuations.

**Image Source Refinitive

Portfolio Commentary

I want to close with a few comments about our discretionary portfolios. The third quarter was frustrating, but it was also one filled with opportunity. Several of our holdings experienced significant price movements in both directions during the quarter, and we traded into those swings where we saw opportunity.

Being a disciplined investor also requires the ability to ignore emotions. Years ago, an investment manager used the image of a child eating peas to describe how it feels to buy when prices are low. This year has been full of those moments for me. Fortunately, many of them have already worked out nicely, including additional purchases of Costco, PepsiCo, and Walmart earlier this year. More recently, we made additional investments in M&T Bank and Chevron, both of which have already rebounded sharply. Some of you may have noticed more recent purchases in London Stock Exchange and FedEx, which are still trading near their lows.

I have spent the past 25 years studying the stock market as a professional investor working on behalf of our clients. I have extreme confidence in very few things, but I do have complete confidence in two maxims. The first is that the greatest losses occur when emotional mistakes are made—whether driven by fear or greed. In today’s market, I am increasingly seeing greed and envy influence decision-making.

The second maxim in which I have complete confidence is that price and quality matter. Periodically, Mr. Market allows speculation to drive the prices of companies with little or no actual profits to unsustainable levels. Eventually, however, stocks trade based on the value of their underlying cash flows.

Our portfolios are built with this principle in mind. We own high-quality businesses with measurable earnings and free cash flow that are trading at reasonable valuations based on their future growth opportunities. While allocations vary slightly across client portfolios, the fundamentals of the stocks held in our core portfolios trade at an average discount of approximately 20% to the index on both a price-to-earnings and price-to-cash-flow basis.

Additionally, our holdings offer higher dividend yields and carry lower levels of debt on their balance sheets. Over time, I am confident that owning higher-quality, lower-priced companies will be critically important for our clients as they work to protect their purchasing power against inflation.

Biggest Outperformers Year-to-Date

- Microsoft

- T. Rowe Price

- Chevron

- J.P. Morgan Chase

Worst Laggards Year-to-Date

- Henkel

- Brown-Forman

- Amgen

- Fed-Ex