The first quarter of 2021 has been a pleasant and largely uneventful period for our portfolios. That is not to say that markets moved straight up or that we have no areas of concern, but rather that this quarter felt far less frenetic than what we had grown accustomed to over the past year.

I’m sure many of you feel similarly about the past eighteen months and are still somewhat astonished by what now begins to feel “normal” in a time like this. As a firm, we are grateful to our clients for allowing us to act decisively during that roller coaster period, which in turn helped generate the returns reflected in this month’s performance reports, currently being mailed.

My intent with this letter is to keep it concise by providing an update on the economy, a brief market commentary, and a recap of our portfolio activity for the quarter. As always, we will continue working to keep your portfolios properly positioned for whatever opportunities may arise.

Economy

The economy continues to improve, though it does not yet fully reflect the reopening that the stock market appears to be discounting. The U.S. economy experienced a record-setting decline of more than 30% in the second quarter of last year, followed by an equally unprecedented 30%+ recovery in the third quarter, as reported for real GDP by the Bureau of Economic Analysis. This was followed by strong—but less historic—growth of around 4% in the fourth quarter of 2020.

The rollout of vaccines, coupled with improving economic fundamentals, is expected to drive very robust growth in the second half of this year. One data point that continues to astound me is the personal savings rate. According to the St. Louis Fed, Americans had a personal savings rate above 10% for the twelfth consecutive month in February. That figure is likely to rise even further as many families received stimulus checks in March and April.

While we anticipate setbacks and unexpected shocks to the economy over the next 12 to 18 months, there is a tremendous amount of new savings available for consumers to spend whenever they choose to do so.

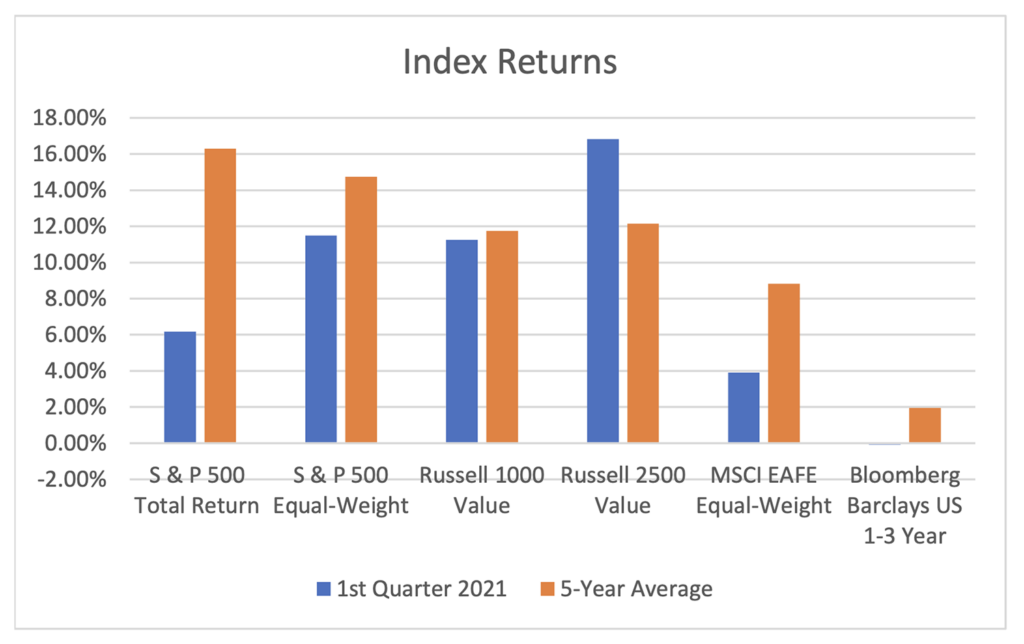

Market Commentary

The first quarter was a continuation of the rally that began just over a year ago for the stock market. Additionally, it was another quarter in which the leadership did not come from the S&P 500 or the FAANG stocks (Facebook, Apple, Amazon, Netflix, Google), which had generally led over the prior five years. The equal-weighted S&P 500 outperformed the cap-weighted S&P 500 index for the quarter by more than 5%. Similarly, the Russell 1000 Value and Russell 2500 Value indices also outperformed the S&P 500 during the quarter. Simply put, the hundreds of companies in the bottom half of the index had a stronger start to the year than the giant technology companies at the top, which represent around 30% of the index’s value.

International equities continue to lag the returns of U.S. markets, and we expect to continue finding attractive opportunities among high-quality companies domiciled outside the United States.

As we have noted previously, we remain concerned that many investors are unaware of the downside risk in their bond allocations if interest rates begin to rise. In an unusual twist, the Bloomberg Barclays U.S. Aggregate 1–3 Year Maturity Bond Index—which we include in quarterly performance reports—posted a very small loss for the first quarter of 2021. This index holds only very short-term bonds, and many investors were surprised to see even these lose value.

The larger Barclays Aggregate Bond Index, which includes longer-dated bonds, posted a more significant loss of 3.4% for the quarter. The Vanguard Total Bond Market Index Fund lost a similar 3.61%, roughly three times its current annual yield of 1.32%. By comparison, the yield on the 10-year U.S. Treasury Note rose less than 1% during the quarter and is still trading below 2%. For reference, the long-term average yield on the 10-year Treasury is closer to 6%. Imagine the potential losses if rates were to return to that 6% level over the next few years.

“The main thesis of this book—that stocks represent the best way to accumulate wealth in the long run—remains as true today as it was when I published the first edition of Stocks for the Long Run in 1994.”

— Jeremy Siegel

Absher Wealth Portfolio Recap

It was a busy quarter of trading for us, but those changes were primarily driven by our intent to manage downside risk. In our Core Model, we addressed two longstanding holdings with clear fundamental concerns and replaced them with companies that we felt had significantly better risk/reward characteristics. In the process, we were able to improve the quality of the portfolio while also enhancing its diversification. The companies that were sold had been in our discretionary portfolios for many years, so we did realize some capital gains.

In the case of 3M, we sold the shares due to concerns regarding their liability related to a chemical known as PFAS. While this issue could ultimately be a non-event, we felt the prudent decision was to exit the holding, as we could not fully assess the potential liability from lawsuits associated with the chemical’s production. We reinvested the proceeds from 3M into M&T Bank, which provides our clients with exposure to more traditional banking, complementing our existing holding in the more capital-markets-focused J.P. Morgan Chase. M&T Bank stands to benefit from a steepening yield curve and the reopening of the American economy.

In the case of Intel, we sold shares after they rallied near 20-year highs amid optimism generated by an activist shareholder. Intel has clearly lost its leadership position in the race to produce smaller semiconductors, with large Asian foundries several years ahead. The future for Intel appears eerily similar to that of IBM. During the quarter, we also added Tokyo Electron Limited to our Core models. These purchases were incremental rather than a single transaction following the Intel sale, but most of the Intel proceeds were ultimately reinvested here. Tokyo Electron is a debt-free Japanese company in the semiconductor equipment industry, which has evolved into an effective oligopoly dominated by five companies. As the global arms race for chip manufacturing intensifies between the U.S. and China, we believe this company will be a clear beneficiary.

The two stocks we sold represented areas in the portfolio where we already had other exposure, and they were both very large American companies. The companies we purchased with the proceeds from 3M and Intel are unique from an industry perspective and smaller in size. This combination added multiple layers of diversification. The average market cap of the two companies sold was four times larger than that of the two we bought. Additionally, we increased our international allocation and added new exposure to semiconductor equipment.

Our portfolios remain focused on owning companies that we believe have a strong margin of safety and possess growth potential at a reasonable valuation. The characteristics we use to identify margin of safety include profitability, balance sheet strength, free cash flow, and barriers to competition.

“In the final chapter of The Intelligent Investor, Ben Graham forcefully rejected the dagger thesis: ‘Confronted with a challenge to distill the secret of sound investing into three words, we venture the motto, Margin of Safety.’”

— Warren Buffett

Closing Comments

I want to conclude this note with a few observations. The stock market has been exceptionally strong over the past thirteen months, and there are clearly pockets of excess speculation. While we see many positives for the economy in the months ahead, we also recognize areas of concern, such as rising inflation and interest rates.

The global economy is reopening, which should drive significant earnings growth. American consumers, in particular, may dramatically increase spending, supported by higher savings balances and improving consumer confidence driven by strong asset growth over the past year.

We make our investment decisions based on the fundamentals of each company—not on economic forecasts. That said, we do consider economic risks, including rising inflation, in our decision-making. Our highest priority is protecting the affluence that our clients have accumulated from inflation and other long-term risks throughout their lives.

Our success requires discipline and patience from both our team and our clients. We remain cautiously optimistic about the year ahead and will exercise discipline and prudence when opportunities arise to improve the quality and upside potential of client holdings.

Performance Attribution Notes:

Core Model (for positions owned for the full quarter):

- Top Performers:

- Polaris +41%

- Deere +39%

- Chevron +26%

- Worst Performers:

- Brown-Forman -13%

- Apple -7%

- Costco -6%

Tactical Model (for positions owned for the full quarter):

- Top Performers:

- Polaris +41%

- Tapestry +33%

- NXP Semiconductor +27%

- Worst Performers:

- Adidas -14%

- Apple -7%

- Walmart -5%

The winners above are generally cyclical businesses who stand to benefit from the reopening of the economy, while the laggards are all high-quality businesses that were less impacted by the global pandemic.