I was reading a speech given by Charlie Munger a few months ago. One of the themes in his speech was that a diligent and observant investor had likely seen it all after three decades of market experience. My 25th anniversary in the industry is coming up in March. Over my career, I experienced the worst calendar year decline for the stock market since the Great Depression. That was 2002 which, as you know, was a short-lived record surpassed in 2008. Those bear markets also qualify as the 1st and 2nd largest cumulative declines since the Depression.

There was the tech bubble prior to those bear markets that included a BusinessWeek cover about Warren Buffett, whom I considered then and now to be the quintessential investor, being over the hill and losing his touch amid the dot-com frenzy. There was the collapse of Long-Term Capital, the Enron and WorldCom frauds, Brexit, and the turnover of Hong Kong to China. I must admit that I thought Charlie might be right. After 24 years of working in the stock market, I doubted whether anything could really surprise me. That was before 2020.

History will remember 2020 for the tragic pandemic that took the lives of millions. The stock market had historic moments as well, though investment returns ended up being one of the few highlights of 2020 for disciplined investors who did not succumb to their emotions during the scarier moments. The decline in the first quarter was the fastest 30% loss for the major stock market indices in the modern era, even faster than the 1987 crash when measured from the closing high on February 19th to the closing low on March 23rd.

It seems unfathomable that those losses would be completely recovered in just a matter of weeks and that 2020 could end with stocks at or near all-time highs. Yet, that is exactly what happened. Despite the resurgence of the coronavirus pandemic, the stock market, as measured by either the Dow Jones Industrial Average or the S & P 500 Index, is finishing the year at or near an all-time high. As a result, Absher Wealth and the portfolios that we manage for our clients are finishing 2020 on a very strong note. Again, it may be the only highlight for many during this difficult year.

I could easily spend this entire commentary revisiting and replaying the roller coaster that was 2020. However, that exercise would do nothing to improve our emotional state nor is it likely to improve our future returns.

“Charlie (Munger) and I don’t pay any attention to macro forecasts. We have worked together now for 54 years and I can’t think of a time when we made a decision on a stock where we’ve talked about macro.

We don’t know what things are going to look like, in any precise way. Why spend time talking about something you really don’t know anything about? People do it all the time, but it’s not very productive. So, we talk about the businesses.”

— Warren Buffett

At the 2013 Berkshire Hathaway annual meeting

Market Conditions and the Outlook for the Future

As I begin discussing the New Year, a question invariably follows about my outlook for the stock market. The stock market is going to be impacted by the reopening of the global economy, but also by unexpected economic or political events, setbacks related to the pandemic, and, most of all, by investor behavior.

Even if we could somehow anticipate the news headlines before they happen, a shift in the mood of investors toward euphoria or back to pessimism would undermine any market forecast that I might make. However, that isn’t to say that investors should bury their heads in the sand and not pay attention. Rather, our job is to be aware of the conditions at hand and be prepared to take advantage of those opportunities that may be created by a surprise to the status quo. In other words, we will do our homework and be prepared for whatever may come our way.

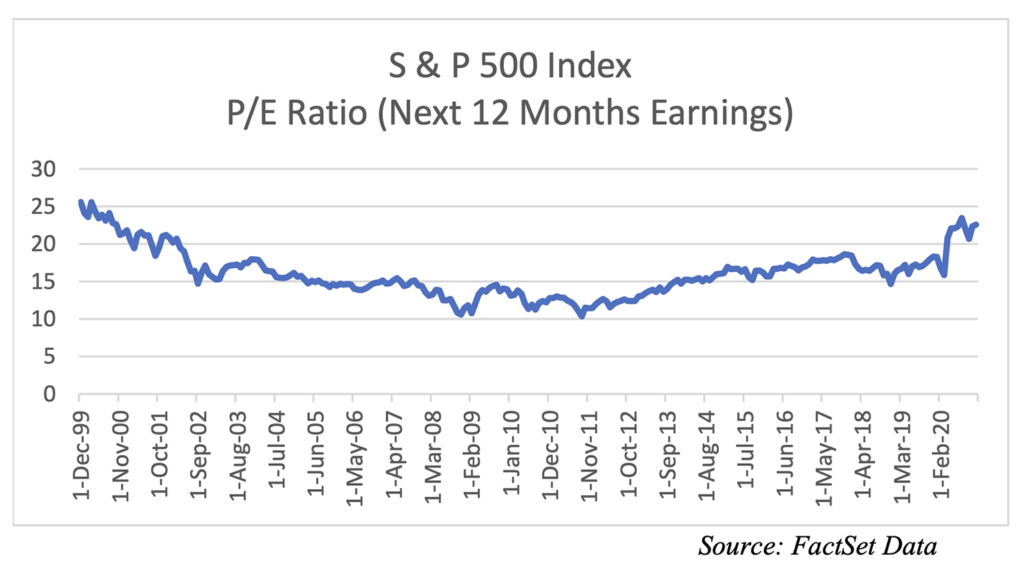

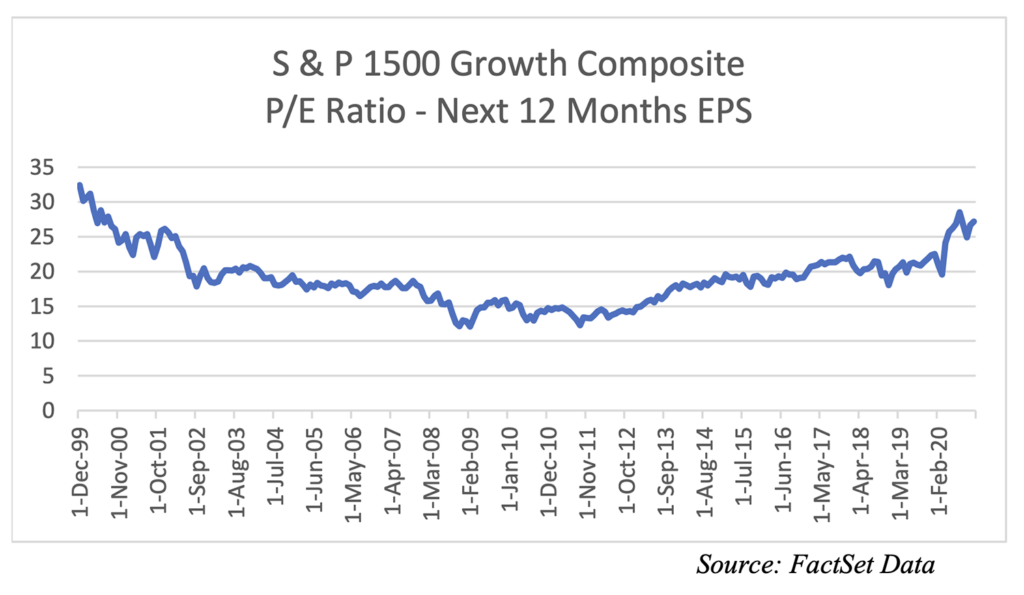

With that in mind, here are the conditions that stand out in my view as we prepare our portfolios for 2021. The overall stock market is becoming more expensive, especially so among the more exciting growth segments of the economy (i.e., technology). We are not back to the valuations of the dot-com bubble, but we are getting closer.

I think it should be pointed out that the trend line on the chart above is heavily skewed by a few very large and expensive stocks (i.e., Amazon).

“History does not repeat itself in the same way each time, but certain trends and consequences are constants.

If you do not know history, you think short-term. If you know history, you think medium and long-term.”

— Lee Kuan Yew

While the overall market does not look as expensive as it did during the dot-com bubble, we do see some individual areas of speculative froth like Tesla. In the chart below, Tesla is compared with other iconic stocks when they traded at similarly euphoric valuations in their moment of glory. History shows us that the market has not always been kind to investors willing to pay any price for a stock.

It is important to remember the old Wall Street adage: the market can stay irrational longer than we can stay solvent. For that reason alone, we never short stocks. However, we also stick with our fundamental discipline of focusing on quality and valuation to provide us with a margin of safety. Our objective is to grow our client capital in the most sure-footed and steady manner that we can. While we certainly desire to make extraordinary gains when we can, we also desire to do no harm along the way. Fundamentals always matter, especially when markets look like they do now.

“To have a true investment there must be a true margin of safety. And a true margin of safety is one that can be demonstrated by figures, by persuasive reasoning, and reference to a body of actual experience.”

— Benjamin Graham

“(Benjamin) Graham’s wonderful sentence is ‘an investor only needs two things: cash and courage.’ Having only one of them is not enough. Courage is a function of the process.”

— Seth Klarman

Important Considerations for our Portfolios in 2021

- Interest rates remain low. Until central banks change course, the alternatives for investors remain limited. While stocks might be a little expensive compared to historical valuation levels, they are extremely cheap compared to bond yields. The 10-year Treasury Bond was yielding just 0.92% on the last day of the year, while our core portfolio had an earnings yield of nearly 5%. Historically, these two numbers would be close to equal, which implies stocks are still cheap compared to bonds.

- We do not own the S&P 500 nor the economy. We own companies and have specifically avoided entire industries and sectors. Our portfolios are not significantly more expensive than their normal historical range based on consensus earnings estimates for 2022. Given my view on the pandemic and the vaccine rollout, we believe our portfolios are very well-positioned for the future.

- The businesses that we own are exposed to the entire world. While we own a few companies that are entirely domestic in nature, the overwhelming footprint of our businesses is more global than the S&P 500. While the pandemic has been tragic in every sense of the word, there will be roughly eight billion people who will welcome the New Year hoping to improve their lot in life. We own companies prepared to benefit from those consumers and their aspirations.

“We aren’t looking at the aspects of the stock. We’re looking at the aspects of a business. It’s very important to have that mindset—that we are buying businesses whether we’re buying 100 shares or the whole company. We always think of them as businesses.”

— Warren Buffett

Closing Thoughts

As we begin the New Year, it is important to remember our discipline. There should be investment opportunities for us as the global economy stabilizes and returns to more normal conditions. There will also be adversity and uncertainty along the way as government supports are removed. Although there are clearly pockets of extreme optimism and even froth in the investment universe, we believe there are still companies trading well below their intrinsic value even now. Historically, the need for a disciplined fundamental approach is most important in markets with similar characteristics to where we are today. Our focus will be on identifying businesses with sustainable competitive advantages that have a global footprint and are trading at a reasonable valuation. The ability to participate in the global economy is critically important as eight billion people adjust to a life after COVID-19, while the awareness of value should provide us a better margin of safety than the broader stock market indices. Given the incredibly low interest rate environment and the exploding levels of government debt, our ownership in outstanding global businesses might be one of the only options capable of supporting a retirement income while keeping up with inflation.

This year has been exceptionally difficult for so many families around the world. Like many of you, our team anxiously awaits the opportunity to return to those daily activities that we all took for granted just a year ago. However, we are all too aware that many families have lost loved ones and those families may feel that nothing will be the same after 2020. I just want to make certain that our clients know how much we appreciate and care for them, especially in a year like this one. We are thankful that we get to do something we love and to do it for people whom we genuinely respect and like.

“Buy not on optimism, but on arithmetic.”

— Benjamin Graham